Driving Defence: The automotive sector’s role as a potential enabler of Europe’s defence surge

Europe’s defence build-up may depend not only on higher spending, but also on industrial adaptation. This paper explores how the automotive sector — facing overcapacity, layoffs and technological transition — could help support Europe’s defence surge by providing manufacturing capacity, skilled workers and dual-use innovation. It also examines the major barriers to closer cooperation and sets out policy recommendations to unlock this potential.

Why now?

-

Geopolitical triggers and increased spending: Russia’s ongoing war in Ukraine and doubts over the US commitment to NATO have spurred a major increase in European defence spending. NATO’s 32 nations agreed at a summit in The Hague in June 2025 to raise defence spending to 5% of GDP by 2035 (3.5% for core military expenditure, 1.5% for defence-related spending). The US is dribbling out announcements of limited troop withdrawals from Central Europe and has ceased funding military training in the Baltic states. More retrenchment is expected.

-

EU financial mobilisation: The European Commission outlined plans in March 2025 to mobilise an additional €800 billion in defence spending over the next decade, including €150 billion funded by Security Action for Europe (SAFE) loans for joint procurement. This seeks to promote a paradigm shift towards a more coordinated and industrially integrated European strategic autonomy. The Commission also activated the escape clause from EU fiscal rules to authorize member states to run budget deficits beyond 3% of GDP to borrow for defence.

-

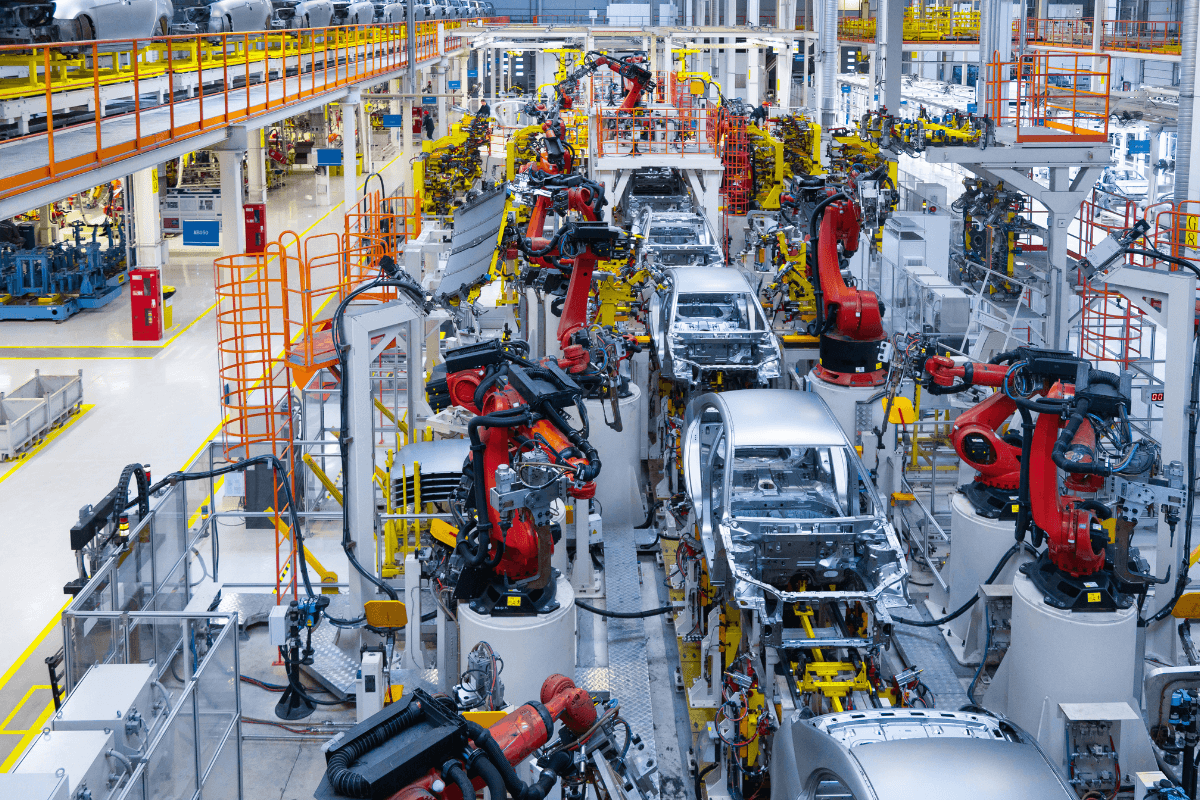

Market opportunity and industrial downturn: The market growth potential in military logistics alone is estimated at well over €50 billion in the next 10 years. This demand coincides with a secular downturn in the European automotive sector, which has significant overcapacity. A survey of six light vehicle producers found average capacity utilisation was just 60% in 2023.

What the automotive sector offers

-

Production and workforce: The automotive sector, which accounts for around 7% of the EU’s GDP and 13.8 million jobs, offers production facilities, skilled workforce, and mass production know-how that the defence sector needs. The industry can act as an enabler of the rearmament drive at a time of uncertainty over its own future.

-

Technology and logistics: Potential collaboration areas centre on military logistics, streamlining and automating manufacturing processes, and developing dual-use technologies, including software-defined vehicles, supply chain resilience, and contingency planning for crisis and wartime.

-

Talent pool: Deutsche Bank analysts argue that the German auto industry has a "historic opportunity to kill two birds with one stone" by turning some of its prowess to military production, leveraging its workforce capacity. The defence sector needs hundreds of thousands of new skilled workers, many of whom are currently in surplus in the automotive industry (e.g. AI engineers, robotics experts).

Key barriers

-

Market fragmentation and regulation: There is no single European market for defence. Companies face an array of obstacles and uncertainties around tenders, contracts, complex country-specific military requirements, intra-European export controls, strict security regulations and certification. EU countries make extensive use of the Article 346 TFU national security derogation from competitive tendering.

-

Business model mismatch: The business models of the two sectors are as different as ready-to-wear fashion and haute couture. The automotive sector is geared to mass production in highly competitive global consumer markets, while defence operates on long-term, low-volume contracts, usually for a single government customer or a handful of national militaries, each with complex national specifications and tight security requirements.

-

Limited business control: Given the complexity and heavy security requirements involved in manufacturing military goods, defence companies are likely to remain the prime contractors. Overall project management is unlikely to be transferred to the automotive sector.

-

Pace and political uncertainty: Most OEMs view defence as a relatively low-volume add-on (1% to maximum 5%) and are thinking only in linear, peacetime terms, lacking contingency plans for potential war. There are significant doubts among OEMs and defence companies about the duration and sustainability of Europe’s rearmament drive, especially if a ceasefire occurs in Ukraine.

-

Cultural constraints: Some OEMs have Environmental Social and Governance (ESG) policies that prevent them from involvement in producing weapons and ammunition.

Strategic recommendations

-

Market access and harmonisation: EU-NATO cooperation is needed to prise open national defence markets, facilitate joint procurement, and enable the free circulation of defence goods within the EU and NATO. Common procurement requires a harmonisation of national defence requirements, military specifications, procurement timetables and certification of equipment.

-

Workforce transfer: Policy instruments such as mobility premiums, reskilling allowances, flexicurity benefits and expedited security clearances should be used to facilitate a managed transfer of workforce from automotive to the defence sector.

-

Financial and regulatory easing: Public policy should support easing EU competition enforcement for defence mergers and acquisitions and collaborative sourcing of critical raw materials. Funding should be expanded for EU programmes like the European Defence Fund (EDF) and the European Defence Innovation Scheme (EDIS) to support cutting-edge crossover technologies.

Read the full Discussion Paper here.

Paul Taylor is a Senior Visiting Fellow in the Europe in the World Programme and a member of the Defence/Security EUrope project.

This paper was produced as part of a partnership between the EPC and ACEA, the European Automobile Manufacturers’ Association.

The support the European Policy Centre receives for its ongoing operations, or specifically for its publications, does not constitute an endorsement of their contents, which reflect the views of the authors only. Supporters and partners cannot be held responsible for any use that may be made of the information contained therein.